Over the last 5 years, I am continuously amazed that when a seller and buyer agree to a price for the company, so many people still get in the way of it happening; and this is after both parties have agreed to the terms of the sale!

This should not be a surprise since so many people involved in the transaction have an incentive for it not to close quickly and actually financially benefit from the delay.

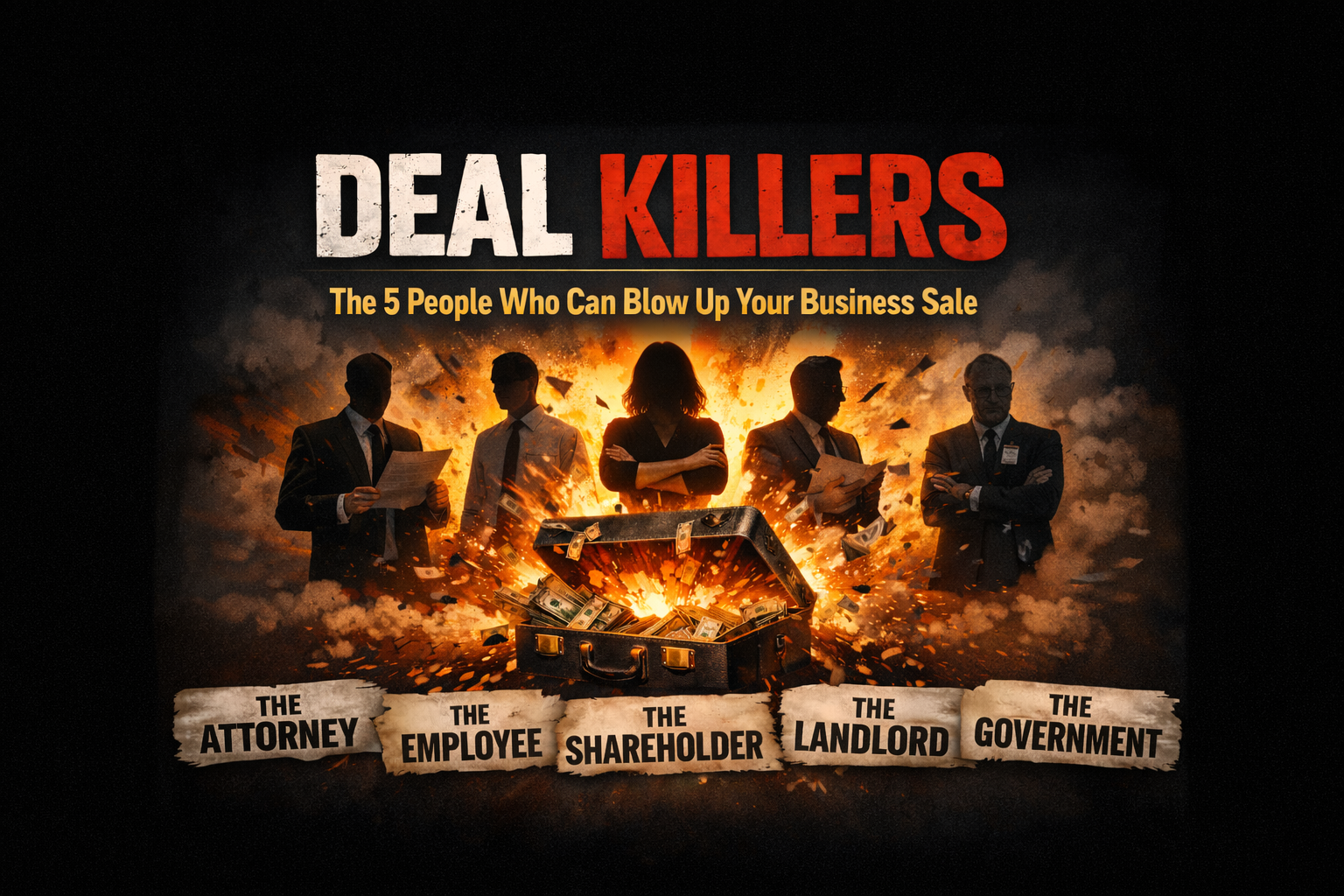

Here are the people that can get in the way of the closing:

- The Buyer’s Attorney

What Happens: Law firms bill by the hour and as a result they have no incentive to close a deal early. Many will bring up an endless amount roadblocks in the name of “reducing the risk” of the transaction. Many will scare the buyer on an ongoing basis. I was once part of a deal where the law firm debated how the transaction would be affected if “the sun exploded”!

My Advice: Hire the right size law firm for your transaction. If you have a million-dollar deal don’t hire a firm that only does $50M deals. Always ask what the approximate fee will be. Hire a firm that will advise you of the risks but not be an impediment to closing by allowing you to make the business decision.

- The Key Employees

What Happens: Many times, key employees are an important part of a deal for continuity. Once employees see how much the owner is getting from the deal, some want “their share” (especially if there are no valuable stock options). I have seen employees refuse to cooperate in the deal or transition to the new company unless they get a retention bonus. My client that sold his company for $100M was forced to give million dollar retention bonuses to 3 key employees to close the deal.

My Advice: Make sure as the business owner, your financial objectives with the sale are aligned with your employees. Be generous. Expect them to get “their share”.

- The Shareholders or Debt Holders

What Happens: Preferred and common shareholders always need to approve the transaction. Many will have lawyers that won’t like the purchase agreement as written and will ask for changes. Some will want a “special treatment” to vote for sale. Debt holders may want a payoff fee to end the loan.

My Advice: Follow the shareholder agreement for any preferences. When threatened by a shareholder for special treatment, hold firm and tell them what will happen to them and the company if they do not sign. Once client once replied to a non-signing shareholder “See you in court”. They signed.

- The Landlord

What Happens: Most leases have a change of control clause which means that the landlord needs to approve the new tenant (the buyer) for the lease. Many times, landlords will hold up there approval to get a transfer fee or try to get the buyer to agree to new higher rates.

My Advice: Stick fast to the clause in the lease that the landlord can’t reasonably withhold their approval. If the buyer has credit worthiness as good as the seller, there is no issue.

- Government regulation

What Happens: Sometimes local, state or federal government agencies need to approve the new buyer. This could be in a controlled industry that requires a license like schools or childcare. It could be in a protected industry like cybersecurity or just because of the size of the deal. I was part of a deal where a government employee asked for an “incentive” to approve the deal. It was sent.

My Advice: Be nice to these regulators as a default approach. Be patient. Get your attorney involved in needed if the “ask” is non appropriate.

What delayed the sale of your small business?